As I shared in previous posts, I currently own two properties in Memphis, TN. For both purchases I borrowed money in the form of a mortgage so that I only paid for part of the costs with my own money. These loans, the monthly mortgage payments, create the largest monthly expense with both properties.

Quick reminder in regard to the numbers behind my investments:

| House A | House B | |

|---|---|---|

| Value | $72,700 | $58,700 |

| Down payment | $14,540 | $23,480 |

| Loan term | 30 years | 10 years |

| Loan interest rate | 5.125% | 7.25% |

| Monthly mortgage cost | $316.67 | $413 |

| Monthly cash flow | $265 | $128.5 |

The total sum of the mortgage payment has two parts to it: principal and interest. Principal refers to the actual amount of money I borrowed. So for house A, I took a loan of 80% of the house cost ($72,700), which comes out to a $58,160 loan that I will need to repay over the course of 30 years. Interest refers to the fee the bank charges, or the cost of this loan. With house A, I will pay a total of $55,842.50 in interest over the course of the 30-year loan. This brings us to a total (principal + interest) of $114,002.50 after 30 years. In other words, I’ll pay back $114,002.50 in return for a loan of $58,160.

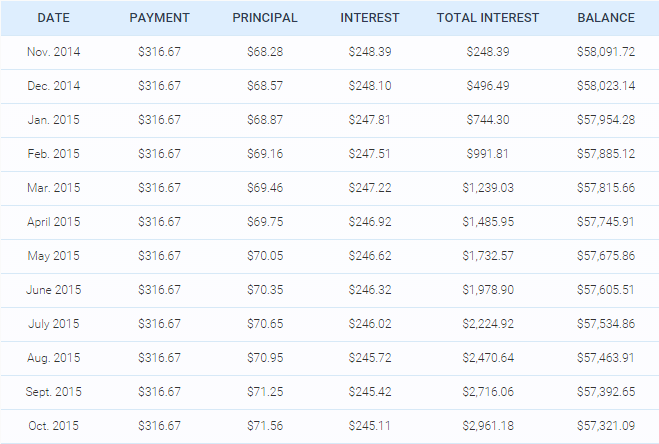

The monthly mortgage payment is always the same amount, for house A the total monthly mortgage payment is $316.67. That amount includes both the principal and interest. What’s interesting is that the amounts change each month. The amount paid towards the principal gets larger each month and the amount paid towards interest gets smaller each month. You can see an example Amortization Schedule sheet below (for the first year of my mortgage on house A). You’ll see the payment made each month, which stays the same at $316.67. Then you’ll see in the next two columns how the $316.67 is broken up into principal and interest. The next column shows the total interest paid thus far and the last column shows the balance or the amount I still owe (principal) on the loan:

If I pay more than the minimum amount, any additional payment goes towards decreasing my principal. Doing this will mean that I will repay the loan back more quickly, and since the loan is being payed off quicker, I’ll be paying less interest.

Let’s look at an example. Let’s look at what happens if I have an extra $50 a month, and I put that $50 toward paying back my mortgage every month (we’ll look at this scenario for each of my properties):

House A

| Original | With extra $50 | Notes | |

|---|---|---|---|

| Mortgage end data | September 1, 2044 | November 1, 2036 | Pay off the mortgage 7.5 years sooner |

| Total interest paid | $55,842.50 | $39,184.23 | Saved $16,658.27 |

House B

| Original | With extra $50 | Notes | |

|---|---|---|---|

| Mortgage end data | December 1, 2024 | November 1, 2036 | Pay off the mortgage almost 1.5 years sooner |

| Total interest paid | $14,398.38 | $12,065.53 | Saved $2,332.85 |

As you can see, with house A, I’d be able to repay the mortgage within 22.5 years instead of 30 years and save $16,658.27 on interest. With house B, I’d be able to repay the mortgage within 8.5 years and save $2,332.85 on interest.

What about cash flow?

Another inportant piece to look at is how much additional cash flow I’d earn by paying off the mortgage earlier. Looking at house B as an example, without paying any additional money each month toward the principal, the mortgage should be payed off within 10 years. But if I do pay an additional $50 each month, the mortgage will be paid off within 8.5 years. This means that I get 1.5 years without mortgage payments and my cash flow will be equal to the net operating income. So let’s see how much additional income I’d receive in those years between when I can pay down the mortgage and when I was originally supposed to pay it off.

| Additional cash flow | |

|---|---|

| House A | $54,712.04 |

| House B | $9,171.37 |

What you can see is that for house A, I’d receive an additional cash flow of $54,712.04 over the course of the last 7.5 years. In other words, instead of paying the mortgage over the course of 30 years and receiving around $265 in cash flow every month, I’d pay off the mortgage over the course of 22.5 years, receive $265 per month and over the course of the following 7.5 years I’d receive a cash flow of around $581.

To pay additional principal, or not to pay additional principal?

To see the full picture, we need to summarize the three main items that will impact the decision on whether or not to pay additional principal:

- Interest saved

- Additional cash flow

- Cost of paying the additional principal

Let’s take a look at these totals for both properties:

| House A | House B | |

|---|---|---|

| Interest saved | $16,658.27 | $2,332.85 |

| Additional cash flow | $54,712.04 | $9,171.37 |

| Amount of additional principal payments | -$13,310.14 | -$5,151.78 |

| Total | $58,060.17 | $6,352.44 |

From this last table you can see that by making an additional monthly payment of $50 on each of my mortgages, over the course of 30 years I will make an additional $58,060 on house A, and over the course of 10 years I’ll make an additional $6,352 on house B.

Let’s do the same thing with amounts higher than $50. We’ll add $100, $150, $200, $250, for each of the houses.

House A

| Extra principal | Mortgage end date | Years saved | Interest expenses saved | Additional cash flow | Extra amount spent | Total savings |

|---|---|---|---|---|---|---|

| $100.00 | June 1, 2032 | 12.26 | $25,357.23 | $85,577.20 | $21,313.97 | $89,620.46 |

| $150.00 | August 1, 2029 | 15.10 | $30,797.19 | $105,369.92 | $26,866.85 | $109,300.26 |

| $200.00 | July 1, 2027 | 17.18 | $34,547.92 | $119,941.95 | $30,812.05 | $123,677.81 |

| $250.00 | January 1, 2026 | 18.68 | $37,300.36 | $130,383.32 | $34,027.40 | $133,656.29 |

| $300.00 | October 1, 2024 | 19.93 | $39,410.89 | $139,122.72 | $36,325.48 | $142,208.13 |

| $350.00 | November 1, 2023 | 20.85 | $41,082.06 | $145,529.05 | $38,524.93 | $148,086.18 |

House B

| Extra principal | Mortgage end date | Years saved | Interest expenses saved | Additional cash flow | Extra amount spent | Total savings |

|---|---|---|---|---|---|---|

| $100.00 | May 1, 2022 | 2.59 | $4,001.12 | $16,699.32 | $8,903.01 | $11,797.42 |

| $150.00 | July 1, 2021 | 3.42 | $5,256.08 | $22,071.37 | $11,855.34 | $15,472.11 |

| $200.00 | November 1, 2020 | 4.08 | $6,235.64 | $26,347.81 | $14,215.89 | $18,367.56 |

| $250.00 | May 1, 2020 | 4.59 | $7,022.14 | $29,599.32 | $16,257.53 | $20,363.92 |

| $300.00 | November 1, 2019 | 5.09 | $7,667.72 | $32,815.48 | $17,713.97 | $22,769.23 |

| $350.00 | July 1, 2019 | 5.42 | $8,207.34 | $34,989.04 | $19,250.96 | $23,945.42 |

What can we learn from all these numbers? Well, the main thing is that we can save money on interest and start earning higher cash flow when we pay additional principal payments. We also pay back the mortgage quicker which means we gain more equity sooner.

The bottom line is that we need to make sure our money is always working for us. As I collect rent and generate cash flow, I watch my bank account grow, but now the question is “what am I doing with the cash flow?” If it’s just sitting in the bank then I’m back at square one. I need to make sure the cash is working for me! To do this, I can use the cash flow in a few ways:

- Invest in new properties. This might take a while as I currently only generate a few hundred dollars each month and would need to wait many months until I had enough for a down payment on a house.

- Invest in the stock market, bonds, etc.

- Pay down the principal as discussed above.

Whatever you choose to do, the key is to make sure the money you’re generating is working for you.

Recent Comments